How to finance your business in the Netherlands

You are starting up a new company in the Netherlands and you have a certain growth expectation? In that case, you will probably need to have some sort of funding. If you are not financing your business yourself, you should look for external funding possibilities.

Luckily, the Netherlands offers a wide variety of funding networks, platforms, venture capital firms, individual investors and of course banks who can help you out. Our own experience shows that it is difficult to get a good overview of the financing options for a foreign small or medium-sized business. That is because there is an enormous number of parties active in the Dutch funding market. On top of that, the focus is on Dutch businesses. This can make it feel like a maze. However complicated it can seem at first, the Netherlands is in fact one of the European countries with best access to funding for small and medium-sized businesses. You just need to know where to look.

There are roughly two types of financing: equity financing and debt financing. Equity financing means raising capital by selling shares in your company. Debt financing means you will find an someone to give you a loan.

Investment or Loan

With an investment you give away a part of your company in return for capital and often the investor's network and knowledge. The advantage of a loan is that you keep full control of your company. With an investment you give away part of your company in return for capital (and often the investor's knowledge and network). A loan, however, will have to be paid back including interest. When it comes to this decision, things are not black and white. It depends on the type of venture, what you are going to use the money for, your personal reasons and many other considerations whether it is best to opt for a loan or an investment. In fact, many startups have both loans and investments.

Below we will try to give you an overview of the Dutch funding landscape. We will go through the most common ways of finding capital for your Dutch business. Plus, we will give you some practical tips on how to deal with the various investors and lenders. Finally, we are always willing to review your business plan and give you some advice. NordicHQ works with a network of partners that provide capital for startups and established businesses.

Business loan at a Dutch bank

Although banks have lost some of their traditional function (and reputation), they are still a key player in financing small and medium-sized enterprises (SME's) in the Netherlands. As a matter of fact, 72 percent of companies with a need for capital will first contact their bank to discuss their funding options. This does not mean that they will eventually take out a loan at the bank, but it nonetheless shows the important role banks still fulfil.

Below are the most important banks that provide business loans for small and medium-sized businesses in the Netherlands:

The most common way of financing these banks provide is either through a bank loan or by providing you with a current account credit. Besides these banks there are several other banks that provide payment services but do not distribute loans and credit.

Most business loans are distributed by a banks. The Netherlands has a well-developed banking system with a small number of large banking institutions. The general notion is that these banks are not very generous in handing out loans to small businesses and especially to more high-risk startups.

A Dutch bank will be mostly interested in two things when granting your business a loan:

- The company's ability to pay back the loan. The bank will look at available cash and cashflow to determine this ability,

- The collateral if the company fails to meet its payment obligations.

This collateral usually consists of assets that the bank can have a claim on if your company fails to pay back your loan. This can be for example inventory, stock or real estate.

It is not always just the above that matters for your business loan application. Other factors, such as your personal experience, your education level and your business plan can also weigh in the process.

Request a free-of-charge quote for a business loan below:

Bank loans and the BV

A BV is a private limited company and therefore a legal entity, separated from you personally. This means that you as an owner are in principle not personally liable for the company's losses and obligations. When granting a loan to a more high-risk business without much collateral to back up the loan, the bank will most likely make sure you personally "co-sign". In case the BV company is not able to repay the loan, the bank will want to make sure that you are personally liable for (at least part of the) outstanding loan.

When you take out a business loan as an sole proprietorship (eenmanszaak) or a partnership (vof) you are already "one" with your company so a debt of your sole proprietorship will automatically be a personal debt as well.

Alternative small business loans

After the financial crisis of 2008-2011, banks have curtailed their services for SMEs, including many payment and lending possibilities. This was reason for several initiatives to fill the gap that the traditional banks left behind.

Both established businesses and startups that are in need of a bank loan but do not meet the bank's requirements, can apply for loans through an organization called Qredits. This is a collaboration between banks and has backing from the government.

Qredits offers a so-called MKB-financiering (SME loan) from €250.000 up to €1.000.000. Besides that, it offers micro-financing up to €50.000. The interest rates are relatively high, but the lending conditions are favourable. For example, there is usually a relatively long interest-free period, to relieve pressure on startups. Besides the purely financial aspects, Qredits offers coaching from experienced entrepreneurs. You will get to choose a coach that matches well with your business.

Convertible Loan

Most banks still stick to somewhat traditional lending methods. On the other hand, more and more other businesses and individuals have entered the business loan market. For them it has become increasingly common to use hybrid forms of funding. The Convertible Loan is the most well-known. Besides the loan terms (interest, payment etc.), the most important topic covered by the Convertible Loan Agreement is the conversion moment. This is triggered when a certain date is reached or a event occurs. At this point the investor can choose to convert the loan into an investment.

This type of loan is often used by startups, because at the very start of a startup it is often very hard to give a realistic valuation of a company.

Convertible loan agreement

Use our convertible loan agreement (also called convertible note) to make your relationship with your lender/investor watertight. The agreement covers at least the following matters:

- The size of the loan

- The interest rate

- The minimum price per share at conversion

- The maximum price per share at conversion

- The discount percentage on the price per share that the investor receives

- In which cases the loan is due and payable in the interim

- In which case(s) the loan will be converted into shares (conversion moment/event)

Public funding initiatives

There are funding initiatives on all government levels that apply to the Netherlands : local, regional, national and European.

As a (starting) self-employed person you can apply for working capital. Different conditions apply for every situation. With a working capital, you can invest in your business. You can receive working capital under the Decree on assistance for the self-employed (Bbz). Usually you receive working capital as a loan. Sometimes you can receive working capital as a gift. That depends on your situation. The application is processed by the local government (gemeente) where you are a resident in the Netherlands.

Regional development agencies (ROM)

Further local initiatives are too numerous to discuss here. What many do not know, is that the Dutch regions are a major driver of investment in innovation. They do that through eight regional development agencies (ROM's). These agencies invest in innovative, fast-growing companies from own funds and other funds under their management. The funds come in the form of subordinated loans or share capital. Take for example InnovationQuarter, the ROM for the province of South-Holland (The Hague and Rotterdam area). They distribute funding through three investment funds worth a total of around €150mln. One of the funds is specifically aimed at CO2 reduction, another invests in innovative businesses in general. You need to be located in the specific region the ROM covers to make use of their funding possibilities. So if you are thinking of choosing a business location, it is worthwhile checking which ROM matches best with your funding needs.

Crowdfunding

Besides the semi-public initiative above, there are several private lending services and platforms. Arguably the most well known is Collin Crowdfund. They offer crowdfunded loans, primarily to established SME´s, growth companies and real estate businesses. An average loan is around €300.000, but they offer much smaller loans as well. Due to the structure with several small lenders, the interest rates are not as high as they are with Qredits and some of the bank loans.

Crowdfunding is usually conducted through an online platform. This is where the entrepreneur pitches his or her proposition including the required amount of funding, to the public. The idea is that many small investors (often individuals, but they can also be professional investors) will participate and together raise what usually would be done by a single or a few investors) will participate and together raise what usually would be raised by a single or a few investors.

A platform worth mentioning is actually one specialized in the selling and buying of companies: Brookz. They do however also offer a possibility to sell or buy part of a business, which makes it relevant for this article. Brookz is a well-established and reliable platform with many relevant advisors and in-house expertise on business acquisition and finding capital. You pay a fixed fee of a few hundred euros after which you are guaranteed response from interested buyers or investors. This makes Brookz one of the cheapest ways to attract capital for your Dutch business.

Informal investors

An informal investor or business angel, is usually a wealthy individual who invests in small businesses. This is often an interesting option if neither own capital nor a bank loan is a possibility. A typical business angel is a former entrepreneur or business person who likes not only to invest but also to share his or her knowledge. So before you attract a business angel, you should be sure that you actually like the person your are dealing with.

This is typically a wealth individual, participating personally or through a personal company. Considering the size of the Netherlands' population there is a relative large amount of these individuals. A business angel does not only contribute his of her money but also brings in knowledge, a network and effort. Angels usually participate in the early stages of a company, often at the very beginning.

If you are not known in the business community in the Netherlands, finding the right informal investor can be challenging. That is why there are several initiatives to organize these business angels in investor networks. BAN Nederland is an example of such a network. Some banks also want to have a piece of this growing investment market. For example, ABN AMRO has set up a matchmaking platform for informal investors and entrepreneurs. A few other platforms and networks that could be relevant:

Venture Capital (VC)

Venture capital is a type of investment that investors provide to small businesses and startups with a large growth potential in the long term. VC's are mostly known for their involvement in funding some of the (now) largest Silicon Valley tech companies. A venture capitalist can be a single individual, but they are often organized in venture capital firms. Venture capital can also be allocated from investment banks or other institutions. Just like many other types of investment, the contribution is not always monetary. Many VC's contribute their kexpertise, knowledge and network to the companies they invest in.

To find the right VC you should first and foremost establish at which growth phase your business is. That is because VC's are usually specialized in one specific funding phase. Roughly speaking there are Seed VC's, Early stage VC's, Later stage VC's and corporate VC's. Find an overview of the VC firms in the Netherlands per growth phase here.

Family office investment in the Netherlands

The Netherlands is a country with many rich individuals and has its fair share of family wealth as well. This wealth is often allocated to be reinvested. This can be any type of investment: from real estate to startups. The goal is often to have a well-spread portfolio of investments with effective growth and to transfer wealth across generations.

Dealing with an investor

Finding an investor is an exciting process. Although we like to focus on the great possibilities a good investor can give you, we need to briefly discuss what happens when things do not go according to plan. If everything goes wrong, an investment is simply gone and the investor loses its investment. In practice, an investor will not simply throw money at your business without guaranteeing any sort of performance obligation from your end. It is therefore crucial that the expectations of investor and entrepreneur are aligned. No matter the exact role of the investor, this relationship should be based on trust. Both parties will have to give and take and realize that things often do not go according to plan.

If the investor is a friend or even a relative, you should be even more aware that both parties have the right expectations. It is always recommended to walk through all scenarios together with a potential investor: what if the success is enormous? but also: what if the worst-case scenario occurs? No matter how close you are to this person, always make sure to formalize your agreement in writing. Unfortunately scenarios will occur that you had not taken into consideration. The best you can do is to make sure your agreement is as watertight as can be.

Preparing for finding capital in the Netherlands

In order to successfully attract investment or obtain a (bank) loan, you will need to have a few things in order. We will go through those things below.

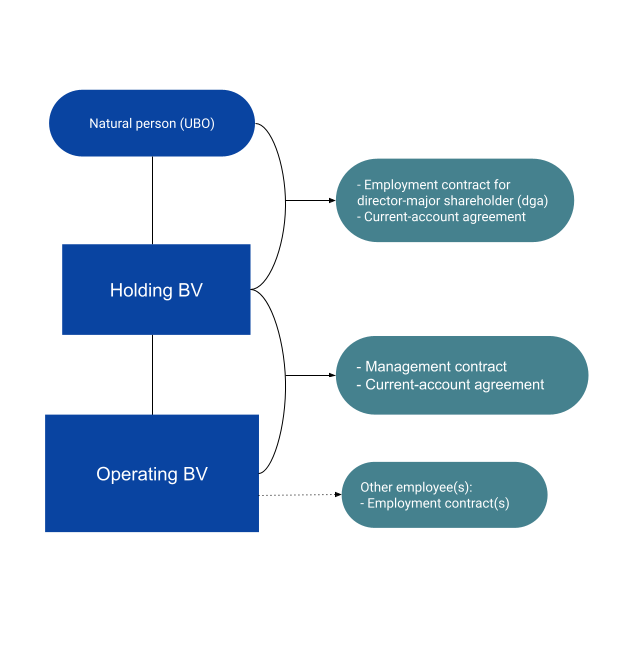

Register the right company entity and structure

First of all, you will need a registered legal entity in the Netherlands. The most investor-friendly legal entity is the Dutch private limited company, or BV. This is both suitable for large businesses and small startups. The main advantage of this entity is that your the BV company is separated from your personal finances. You are not personally liable for the company's actions and losses.

Secondly, if you are ever considering an investment, most investors prefer a BV over another type of entity. The BV consists of a certain number of shares, owned by one of more shareholders. The BV is designed to attract investment and new partners and, if relevant, sell them out again.

Thirdly, a BV can easily be structured in a BV holding structure. This means in effect that every shareholder has its own holding BV, owned for 100 percent by the shareholder. That holding will in turn participate in the operating BV, where the actual business activity takes place. Not only is this holding BV an interesting vehicle for the business' founder(s), it also is for investors. This has everything to do with the Dutch tax system, where dividends from the operating BV can be distributed to a holding BV free of tax.

Let's say that an investor or founder sells his or her shares in the operating BV. In that case, the entire sum of the share sale will flow into the holding BV without having to pay dividend tax or additional profit tax. The idea behind this is that the profit has already been taxed with corporate tax in the operating BV, and this prevents double taxation. The moment one starts paying out the accumulated wealth in the holding BV to himself, you will be taxed with so-called Box 2 tax. This is why wealth is often built-up in a founder's or investor's holding BV. From this holding, it can be reinvested in any other company, without every being taxed.

At Legalee we are specialized in setting up companies for foreign entrepreneurs in the Netherlands. We guide you through the company formation process and help you with all your legal paperwork. We go further than that and help you finding a network, business partners and explore funding possibilities.

Write a business plan and financial projections

A great business plan does not only convince an investor or lender to give or borrow you money, it will get you in the room in the first place! And that is exactly your goal. Most investors will focus on you as a person before they really start digging into your business plan. It is trust in you as a person and your ability to execute your plan that matters most.

It is not set in stone what a good business plan looks like. This means you can organize it as you wish. You will need to be able to identify the most important goals and challenges for the business to reach those goals. On top of that, it can be very helpful to work out a plan with different scenarios.

General tips:

- Avoid unnecessary amounts of text and explanation - stick to-the-point.

- Make sure your goals and objectives are SMART: Specific, Measurable, Assignable, Realistic and Time-related

- Start with a one-page business plan. Make this the first page of the business plan. An investor who does not bother to read the entire thing can still get a good idea of your business with that one page. An alternative is to use the so-called business plan canvas. This is a tool that helps you to write in short what your plan is all about, who your customers are, how you will reach them etc.

- Customize your plan based on the institution or investor you are sending it to.

- Ask for feedback from people who can give you honest and critical feedback.

- Be realistic and honest. Do not include projections and graphs with unrealistic growth. Remember that most investors and especially banks are looking for stable and durable growth, not for taking enormous risks.

The business model canvas is a very helpful tool to establish what your business is really all about

Term sheet

Before you formalize the agreement about an investment the first step is a so-called Term Sheet. This is by no means a mandatory document, but it helps both parties to put their negotiated terms on paper. Most of it is non-binding. A term sheet basically contains the agreements made about the amount of the investment, the shareholding to be acquired and the investor's participation. A term sheet normally precedes a participation agreement. The participation agreement contains the final agreed agreements regarding the investment.

What does a Term Sheet contain:

- the size of the investment;

- the equity interest;

- investor participation;

- confidentiality;

- the deadline for signing the participation agreement;

- which decisions can only be made by the shareholders' meeting;

- exclusivity of the negotiations;

- optionally a drag-along arrangement;

- optionally a tag along scheme;

- optionally an offer obligation, an anti-dilution clause, and preferential rights.

Formalize the investment

After the negotiation phase where you have worked out the main issues in a term sheet, you will move on to formalize your agreement with the investor. A participation agreement is a useful tool to this end.

Participation agreement

A participation agreement contains the agreements about an investment in a private limited BV company. These agreements are made between the shareholders in that BV and the investor(s). In the contract you arrange, among other things, the agreements about the amount of the investment and the share interest that the investor receives in return.

Foreign investment in Dutch company

An increasing amount of foreign investment flows towards Dutch companies. Many of our clients are non-Dutch or non-residents. Therefore many have connections in another country and subsequently attract foreign investment to their Dutch company. We strongly recommend you to contact your bank before that investment from abroad is transferred into your company's bank account. The bank has an increasingly important role in prevention money laundering and terrorism financing under a law called the Wwft. On top of that, you should let the bank know if there is a change in ownership structure. This ownership is first processed at the notary and registered at the chamber of commerce in the UBO register, but should also be communicated to your bank. We advise you to do this well in time, because it might take some time to arrange the necessary paperwork.

Foreign direct investment (FDI) in and out of the Netherlands

At NordicHQ we specialize in guiding foreign entrepreneurs in their business journey to the Netherlands and the rest of northern Europe. Do you have any questions about the above or would you like to get in touch to discuss your options, please fill out the form below or send us an email or use the form below.